Your clients hear from you once a year, and then… nothing

Most advisors default to one of two modes: a dense quarterly market recap that reads like a fund commentary, or complete silence between annual reviews. Neither is working. Client engagement data consistently shows that communication frequency is one of the strongest predictors of whether a client stays, refers someone, or quietly starts taking meetings with other advisors.

A YCharts survey found that 77–81% of clients would be more confident in, more likely to stay with, or more likely to refer an advisor who communicated more often or more personally. That figure was highest among clients with over $500k in assets, which is the exact segment most advisors are trying to keep.

The two things that stop advisors from fixing this are the blank page and compliance anxiety. This guide addresses both, starting with compliance, so you can write without second-guessing every sentence. It also covers what to actually write across the 11 annual touchpoints that turn a once-a-year relationship into something clients actually feel. (For the wider email playbook — list growth, automations, deliverability — see our email marketing strategy guide.)

Newsletters are compliant by default, until you do one of three things

Nothing in this section is legal advice. Your compliance officer and your firm’s supervisory procedures govern what you can send. That said, here is how the rules actually work, because they are less restrictive than most advisors assume.

FINRA Rule 2210 classifies a newsletter sent to more than 25 retail investors as a “retail communication,” which requires principal approval, fair and balanced content, and recordkeeping. That sounds like a lot, but most firms already have a review workflow for exactly this. You submit the draft, someone approves it, you send it. The SEC’s Marketing Rule adds prohibitions on false or misleading statements and specific conditions around performance data, testimonials, and third-party ratings.

What trips advisors up is not the educational content, it is the three categories regulators consistently flag: recommending specific securities, referencing past specific recommendations without proper context, and promoting your own results or services without required disclosures. Stay off those three, and a newsletter covering market context, tax deadlines, planning concepts, or life event reminders is well within normal operating territory.

The SEC’s 2025 exam observations flagged missing disclosures and inadequate oversight, not advisors writing about Roth conversions or year-end checklists.

What to actually put in the newsletter

Once you know you’re safe to write about something, the harder problem is deciding what that something is. Four categories cover most of the best advisor newsletters.

Market context

The goal is not to predict anything. Clients need help understanding what is happening and why their portfolio is not in freefall, not a forecast you might get wrong.

That framing unlocks a lot: a piece comparing the current drawdown to 2011 or 2018 (what triggered it, how long it lasted, what happened after), a plain explanation of why bond prices move inversely to yields for clients confused about their fixed income last year, or a note on how a higher-rate environment changes the math on cash versus short-duration bonds. Historical context lives here, not forecasting.

Financial planning and life events

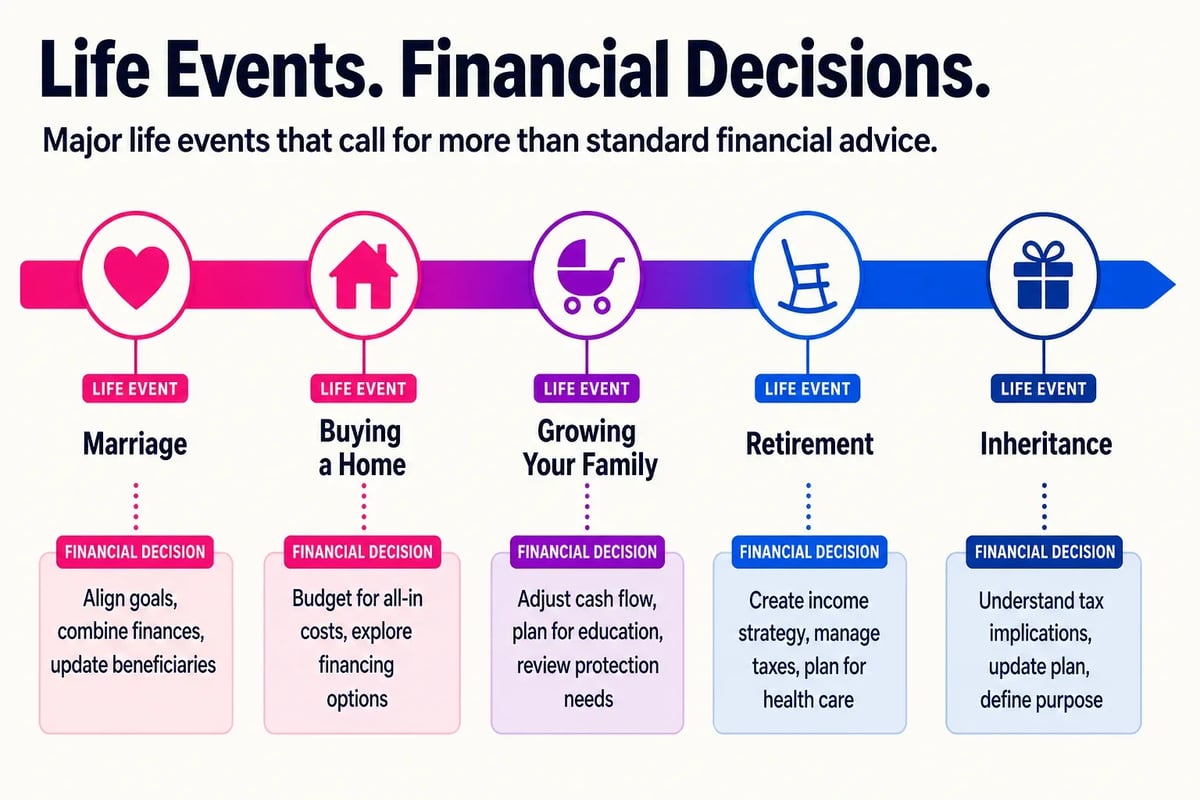

This is the most underused category. A client getting married, inheriting assets, navigating a job change with equity compensation, or approaching Medicare eligibility is not going to google their way to good decisions. A newsletter that walks through what questions to ask when a parent dies, or what to do in the first 90 days after retiring, is useful in a way market commentary rarely is.

Tax and regulatory updates

Deadline reminders, contribution limit changes, rules your clients probably missed. The SECURE 2.0 super catch-up provision for ages 60-63 is a real example: most clients who qualify have no idea it exists. Two paragraphs explaining what changed and what they should ask you about is exactly the content that prompts a reply.

Firm and relationship content

What you have been thinking about. A question three clients asked you in the same week. Why you approach Roth conversions the way you do. A note that you are accepting introductions in a particular situation. None of this needs a compliance review the way performance claims do, and it does more for the relationship than any market update will.

What you get for $200 a month isn’t always a newsletter

FMG Suite is a real product that does real things, and plenty of advisors use it without complaint. But its All In One plans run from $178 to $834 per month, and what you get at most tiers is pre-written content built to work for any advisor, which means it sounds like it was written for no advisor in particular. Reviewers on G2 consistently flag the same issue: the templates are generic, the voice is flat, and clients who receive newsletters from two different advisors on the platform sometimes get the same article. That sameness is a structural feature, not a bug — compliance-pre-approved content has to be broad enough to clear review across thousands of users. Writing your own newsletter, even a short one, sidesteps that entirely. Clients recognize a personal voice. They do not need to be told it’s a template to feel the difference.

Monthly is the floor, not the goal

Most advisors see their clients once a year for a formal review. That meeting carries a lot of weight, partly because it’s often the only structured contact clients can count on. A monthly newsletter gives you 11 more touchpoints before the next one arrives.

Industry guidance commonly cited around 18 touchpoints per year to solidify client relationships, combining reviews, newsletters, check-in calls, and seasonal outreach. Twelve monthly emails don’t get you there alone, but they form the backbone everything else attaches to.

Quarterly is workable if monthly feels impossible right now, but four issues a year leaves long gaps where clients have no contact from you at all. That silence isn’t neutral.

One practical note: consistency matters more than frequency. Starting at monthly and staying there is better than committing to weekly and dropping off after six sends.

Seven subject lines your clients will actually open

The subject line decides whether the newsletter gets read or deleted. These seven patterns work for advisor-client email, adapt the wording to fit your voice.

- “Is your portfolio ready for Q4?” — A question aimed at something the client already cares about creates a small pull toward opening.

- “What I’m watching in the bond market this fall” — Personal and seasonal. “I’m watching” signals a human wrote this.

- “3 things to do before December 31” — Numbers promise a short, finite read. Busy clients respond to that implied contract.

- “A question I keep getting from clients right now” — Implies relevance without giving away the answer.

- “Your year-end checklist” — Ownership language makes it feel prepared specifically for the reader.

- “What the Fed decision actually means for you” — Translates a news event into something personal. “Actually” signals you’re cutting through.

- “We added someone to the team” — Firm news with no hype. Clients who trust you are curious about your world.

Keep lines under 40 characters when possible so the hook appears before the subject truncates on mobile.

What a real advisor newsletter actually looks like

Sample newsletter issue. Adapt the voice, figures, and firm details before sending, and have compliance sign off before distribution.

Westbrook Wealth Letter, November 2025

What the market has been doing (and what I’m not doing about it)

The 10-year Treasury oscillated between 4.0% and 4.5% for most of 2025, the Fed held rates higher for longer, and geopolitical noise did what it always does.

I’m not making portfolio changes in reaction to headlines. I am reviewing liquidity, checking whether tax-loss harvesting makes sense before December 31, and looking at whether allocations have drifted. Moving to cash in a down market usually means sitting out the early weeks of the recovery, which is where a lot of the gains happen.

limit is $23,500, with a $7,500 catch-up at 50+ and up to $11,250 for ages 60-63.")

Your year-end checklist

If you’re 73 or older, your required minimum distribution must come out this year. First-year RMDs have until April 1, 2026, but waiting creates a double-distribution year. The 2025 401(k) limit is $23,500, with a $7,500 catch-up at 50+ and up to $11,250 for ages 60-63. Roth conversion windows close December 31. Beneficiary designations override your will — five minutes to review.

A question I keep getting

“Should I be worried?”

Maybe, about the right things. Your emergency fund, your allocation relative to your actual risk tolerance, and your tax situation before year-end all deserve attention. Whether the S&P finishes up or down this quarter doesn’t. Major life changes this year — a job transition, an inheritance, a family situation affecting your estate plan — that’s what I’d want to talk about.

From the office

We moved to a new scheduling system in October. Book your year-end review at [calendly.com/yourfirmname], or just call.

Frequently asked questions

What should a financial advisor newsletter include?

A financial advisor newsletter should include market context, planning reminders, tax or regulatory updates, life-event guidance, and firm relationship notes. It should educate clients without making unsupported predictions or individualized recommendations.

How often should financial advisors send a client newsletter?

Monthly is the best baseline because it creates regular touchpoints between annual reviews. Quarterly can work as a minimum, but it leaves long gaps where clients may not hear from the advisor at all.

Are financial advisor newsletters allowed under compliance rules?

Yes, advisor newsletters are generally allowed when they follow the firm's review process and avoid misleading claims, unsupported performance references, specific securities recommendations, and missing disclosures.

What financial advisor newsletter topics are safest for compliance?

Educational topics are usually safest: year-end checklists, contribution limits, Roth conversion considerations, retirement deadlines, Medicare timing, beneficiary reviews, and plain-English explanations of market context.

The part that takes the longest isn’t the writing

If you already know what you want to say, the blank page is still the bottleneck. The Newsletter Generator works the other way: you drop in your market notes and a few topic ideas, and it produces a complete draft in your voice. Editing a draft takes 20 minutes. Starting from nothing takes an evening. It’s built with compliance guardrails in mind, so the output gives you something your reviewer can actually work with rather than something that needs to be rebuilt from scratch.